.png)

Smaller Banks Have One Big Advantage to Steal Customers from the Big Guys.

We surveyed 400 consumers to find what makes people stay, and what makes them walk.

Thousands of whitepapers have answered this question. Once or twice, our agency has answered it for our financial services partners.

And every time we get an answer—features, rates, incentives, tech, personalization—every player in the category races to copy what’s working. We end up in the same place we started.

Every. Bank.

Looks. The. Same.

I think we’re asking the wrong question. We should be asking who switches banks.

There’s not a lot of great data on this topic, so we ran a 400-person study through the Brand Joy Lab to understand the consumer at the center of this problem.

Almost half of the respondents told us they had, or had considered, switching banks in the last year (only 9 percent made the jump, which falls in line with industry research).

We went beyond demographics to understand the emotional stakes of switching. The findings tell a story of Americans who are falling short of their own expectations but have hope that a great bank—yes, a bank!—could change things.

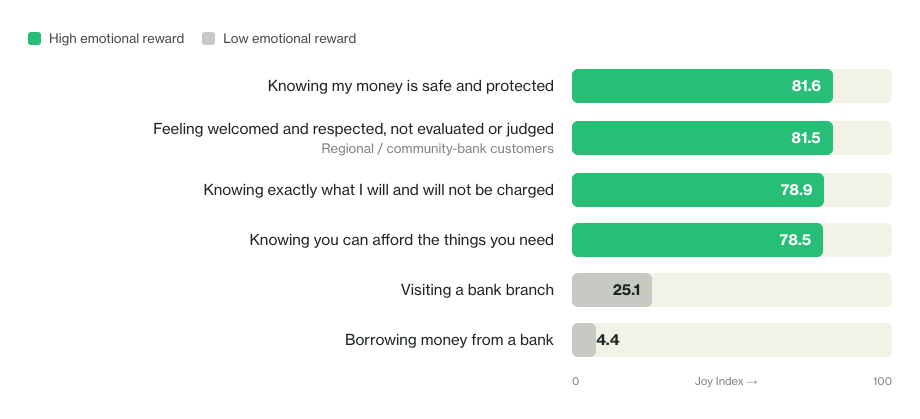

The Joy Index, by banking moment

Source: PETERMAYER Brand Joy Lab, 2023–2026 · n=401–2,138

When people describe the joy their bank brings them, peace comes up most. Security. The feeling that someone has their back. Ask those same people about taking out a loan and the emotional register flips entirely. The distance between those two experiences, between banking as shelter and banking as transaction, tells you everything about the job people actually want done.

A Millennial earning under $25,000 a year described what a good banking relationship felt like:

Encourage and remind me every day of the tools to use. Remind me to keep saving because it's worth it.

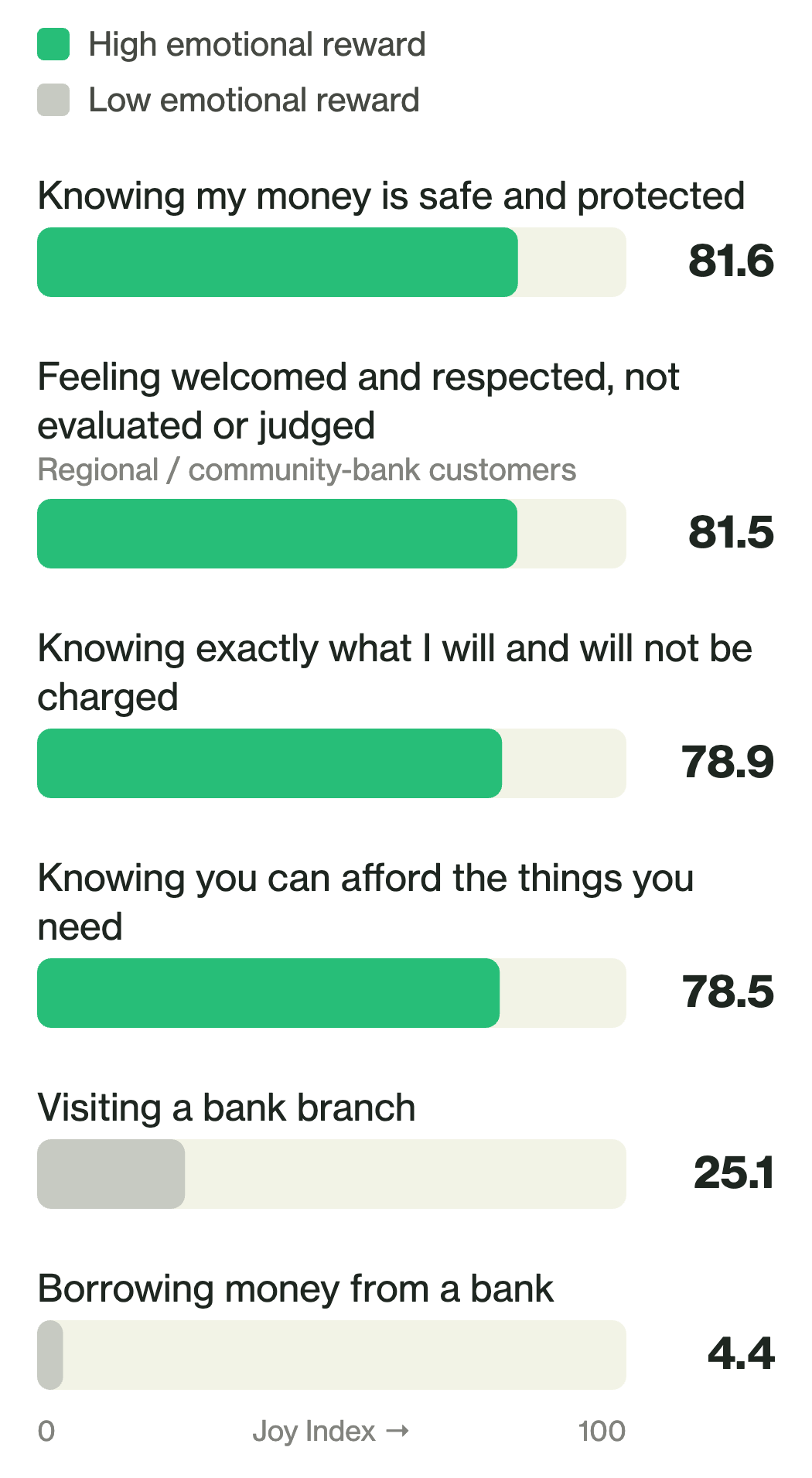

Feeling behind, and feeling things can change

Source: PETERMAYER Brand Joy Lab, 2026 · n=401

The customers most likely to switch banks aren't just shopping for a better rate. More than half feel behind where they expected to be at this stage of life, and they still believe, at nearly the same rate, that the right banking relationship could change their trajectory. That combination of pressure and belief moves people.

A Gen X man in the survey described what he wanted from his bank in three words: “To understand me.”

The customer who considered switching and stayed put registers lower on both optimism and satisfaction. Not desperate enough to act, not convinced enough to go looking. They’re parked in a relationship, waiting for something to change.

How my current bank delivers against my needs

Source: PETERMAYER Brand Joy Lab, 2026 · n=401

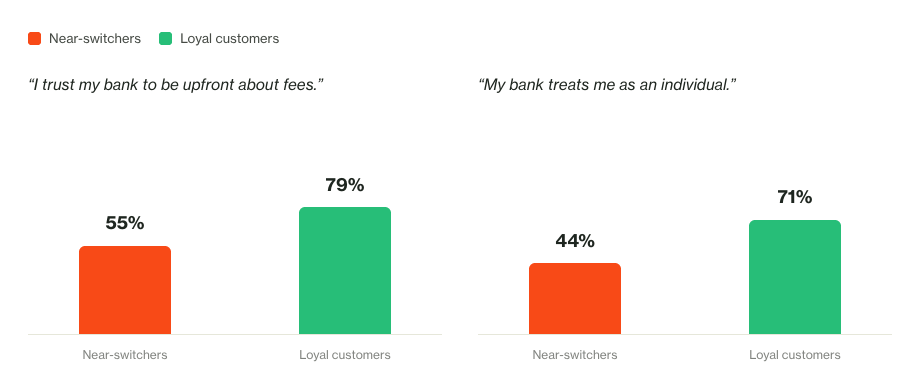

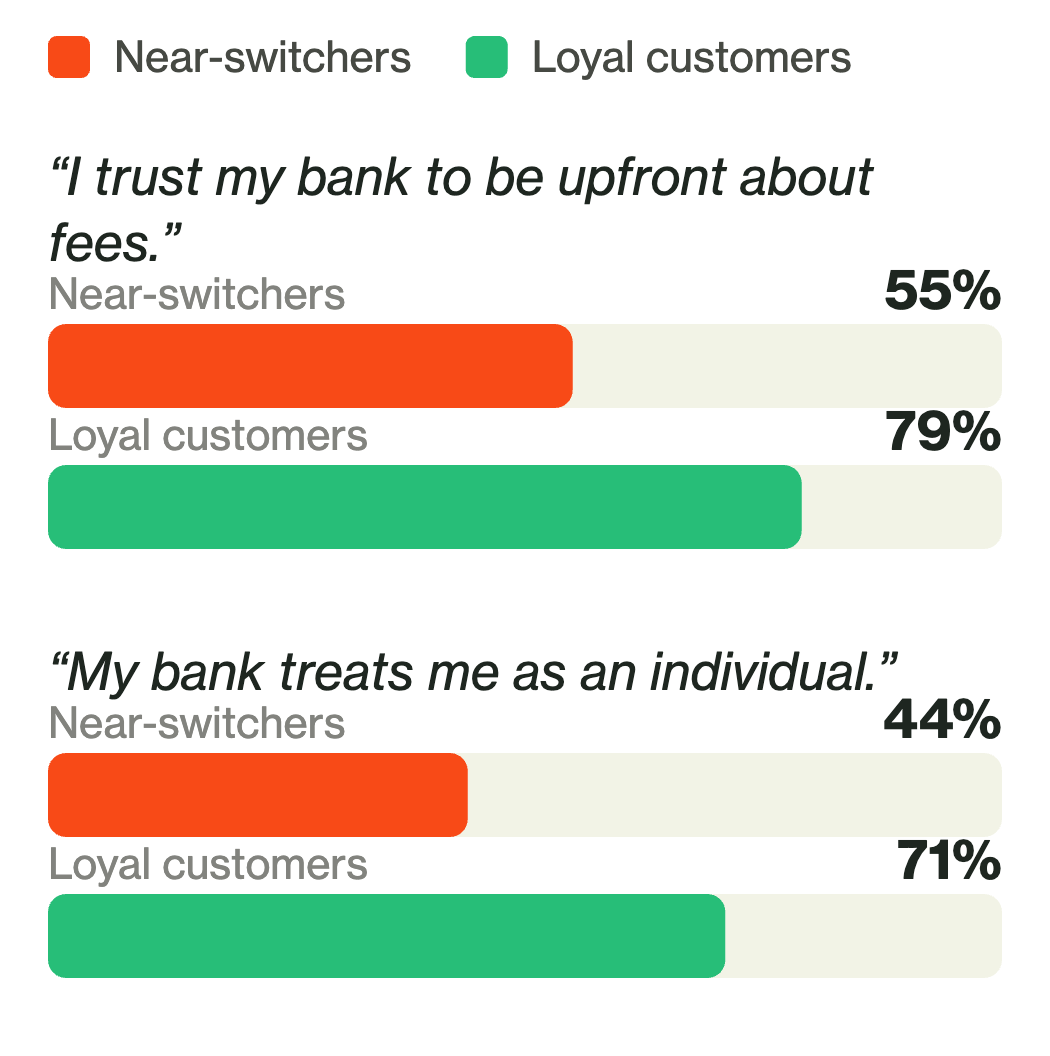

The customer most worth reaching already wants what a community bank offers. Near-switchers rate low fees and the ability to speak to a real person as their top two priorities in a banking relationship.

A Millennial woman from the Midwest described what she wanted: "More personalized guidance, clearer tools to improve my finances, and greater transparency on how I can grow financially with them."

She hasn't switched yet. Nearly one in four actual switchers cite a frustrating or disappointing experience as the final trigger. That moment arrives eventually. The regional bank that has already made itself visible gives that customer somewhere to land when it does.

These banks don’t treat community involvement as a line on their website. They invest deeply in telling and promoting the stories of their people and the ways of life of the communities they serve.

Frost Bank | Texas

A challenger-brand identity that helped a regional bank stand out and grow deposits.

Legends Bank | Tennessee

An internal volunteer program that shows up when it matters most.

The banks doing this well aren’t outspending anyone. They’re just clearer about what they are, and consistent enough to prove it. For a regional or community bank with an honest story to tell, your point of difference lies in your people—both customers and associates.